|

Growing EdTech Trends in Southeast Asia

Compared to other regions around the world, Southeast Asia (SEA) has been known for placing great importance on education. With a notably higher education spend per household, parents in SEA often enrol their children into tutoring or after school learning programmes to give them a competitive advantage amongst their peers.

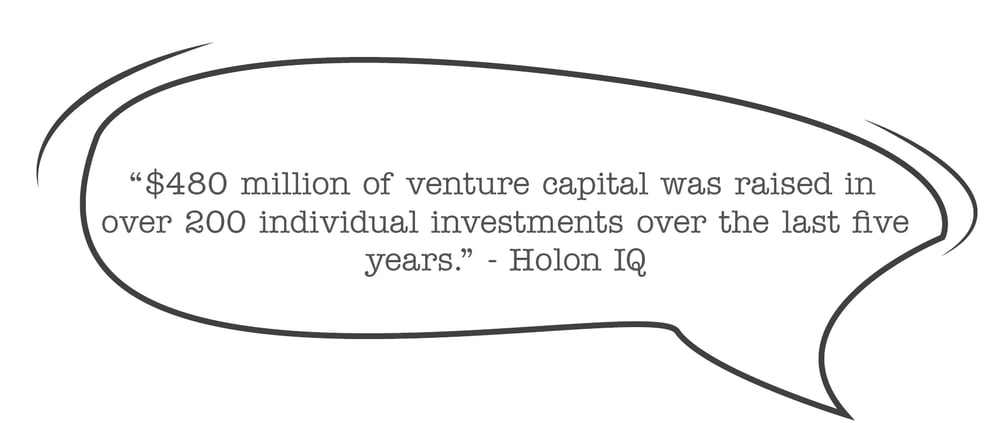

This dedication from parents is coupled with the wider SEA region having the highest internet adoption rates with over 97 million smart devices being purchased in 2019.1 Investors are also taking notice of the SEA region; raising $480 million in venture capital for education companies and enabling the expansion of an already booming EdTech ecosystem.

When the pandemic was declared by the WHO in March, the number of education app downloads in SEA surged 90% compared to the weekly average in the last quarter of 2019. As educational institutions closed, many turned to EdTech solutions in remote teaching and online learning. In SEA, this rapid EdTech adoption was mainly driven by mobile apps, streaming videos, online quizzes and tutorials.

However, the impact of COVID-19 on education created opportunities for EdTech to expand into other areas of innovation. Bhima Yudhistira from the Institute for Development of Economics and Finance in Indonesia shared in a recent interview: “EdTech is still in uncharted territory with a few players and plenty of potential. It is also very segmented, as each level of education needs a different approach; that is what makes it interesting. In the future, EdTech platforms could offer Learning Management Systems (LMS) through B2B partnerships with education institutions. There is also an opportunity to create tailor-made digital solutions and IT system development." 2

However, in rural parts of Southeast Asia, the lack of development and scarcity of trained teachers results in education not reaching all students. Prior to the pandemic, classes had a large student-to-teacher ratio, which further limited students from gaining a high-quality education. With EdTech becoming increasingly accessible, physical barriers to quality education, like distance and lack of school facilities, are removed.

During the COVID-19 outbreak, Ruangguru, the largest tutoring platform in Indonesia, assisted over 7 million users through tutoring videos, tests and homework assistance via their website and mobile app.

In Thailand, Singapore and Vietnam, Taamkru facilitated preschooler lessons using gamification in English, Maths and Science to enable an improvement of 27% in their app test scores over a 15-day period during the pandemic.3

Vietnamese EdTech startup Yovel created a novel online-to-offline education model to assist in remote learning, which aimed to attract students to training centres in Hanoi and Ho Chi Minh City as schools began to reopen.

As technology, internet and personal smart devices are adopted at an increasingly high rate across the region - accessibility of high-quality education will continue to improve. With the SEA EdTech ecosystem constantly adapting and growing during the COVID-19 pandemic, there is an increasing possibility that it could begin to compete with some of the largest global EdTech markets.

1 CNBC

2 Tech Wire Asia

3. Borgen Project

|