|

|

|

|

|

|

In this month's X Report, we look at the role of AI in measuring skills and explore the EdTech ecosystem in India. Each month, we will share a snapshot of key trends, showcase the stars of today and tomorrow, provide some food for thought as well as mergers, acquisitions and fundraising.

|

|

|

|

|

Can AI Measure Human Skills?

A well known driver of education is to help people develop skills and drive human capital. The second element of education is its role in signalling skills to the labor market. The successful bridge between education and work relies on companies understanding what skills matter to their productivity and what skills are achieved within education.

With the increasing pace of technology and lifelong learning, educational institutions are moving towards becoming insufficient in their ability to selectively signal skills. The scaling of online education also allows mass accessibility to high quality education in a way that traditional brick and mortar education can not. However, without selectivity, the question remains as to whether it can compete with traditional education credentials and it’s signalling value. Answering this will rely on whether we can credibly measure the skills that people have and how that translates to productivity in the role.

The hiring process is often reliant on a single piece of paper however, increasing forward thinking companies are realising the long-term challenges in relying on one source of information and so have moved to tech-enabled solutions to help create a more holistic profile of candidates that puts data first.

One example is DBS Bank. The talent acquisition team created JIM (Jobs Intelligence Maestro) that could conduct candidate screening for wealth planning managers, a high volume job in the consumer bank. JIM was able to shorten candidate screening from 32 minutes to 8 minutes, improve the job application completion rate to 97% and respond to 96% of candidate queries. Hilton is another company which accelerated their speed to hire by 85% through using AI in sourcing, screening and interviewing candidates in their hiring process.

Adapting to skills-based hiring will lead to altering job descriptions and potentially the removal of a degree requirement altogether. However, this will also require a mindset shift on how companies select skills. Across all industries, adopting a skill-based hiring approach will need to identify benefits and barriers of widening the talent pool and redeveloping strategies in the hiring process. Focus will also lead to educational and learning pathways to upskill a more diverse employee population.

The challenge in using AI is to successfully source and measure skills. It can be argued that measuring skills is not required to measure a skill, rather measure a task. Because of inability to measure a task at a high level we find proxies to help, these being the skills. For example, in a football game players can be judged on their ability to score a goal. However, measuring their performance can only be achieved in matches. These are often scarce and players are generally on the bench rather than on the pitch. Therefore, how can you continue to assess the player’s abilities when they are not giving the opportunity to play? Rather, their skills are measured in terms of shooting with accuracy and speed, assisting goals and fitness. Our intuition tells us that their ability to perform these different unique skills correlates to the striker being able to score goals in a match. These individual skills are easier for a human and also a computer to measure and assess.

There is still a long way to go for computers to successfully build this type of assessment on individual skills and link them to tasks. The ability to measure soft skills over hard skills and taking hard skills apart to determine a common language in assessing candidates needs to be achieved first before they can be accurately measured. However, it seems co-bots continue to infiltrate the future of work…

|

|

|

|

|

|

EdTech in India

As in many countries around the world, EdTech adoption has been accelerated in India amidst the COVID-19 outbreak. With everyone forced to move to learning online, it provided opportunities for EdTech companies to meet the increasing demand. In June 2020, the Ministry of Human Resource Development in India estimated that EdTech expenditure would be $10 trillion by 2030.

The differentiators between the different EdTech offerings will be language, syllabus, pricing, pedagogy, offline support and teacher training. 22 languages are spoken in India and one key challenge for EdTech adoption is reaching the remote communities in the country. Now that the pandemic has decentralised education, the challenge is to deliver high quality education in local languages and dialects through online platforms. It may be that soon we will see a hybrid approach, with online learning and a live mentor/mentee approach nearly to provide support and reassurance to the student. By having centralised versus decentralised models students can succeed in their education at the right time. It cannot be a one size fits all market and distribution is key. This is something that BYJU mastered, successfully reaching the end customer and using a freemium model.

While K-12 used to dominate the EdTech market in India, K8, STEM and coding are now becoming more prevalent. The government also recently announced that 40% of a higher education course can now be provided online and with an exam driven culture, exam preparation and revision support companies are on the rise. Professional learning has also greatly increased with learning times in India increasing 250% since the pandemic started.

While many have welcomed the increased use of EdTech in India, the market is still complex and fragmented. 60-70% of the population still do not have access to internet or devices. While this is starting to improve with investment allowing the supply of hardware and infrastructure required, still more needs to be done. One alternative being explored is microfinance projects that create library style solutions, to help accessibility in remote areas.

Overall there is vastly increased growth for the Indian EdTech sector, likely to reach $4bn by 2022. The upskilling segment has seen a huge increase and the K12 market continues to dominate, with greater adoption of EdTech by schools and tuition centres. The key drivers and differentiators now for the EdTech market will be curriculum, pricing and offline support, with hybrid approaches to education soon becoming the norm.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

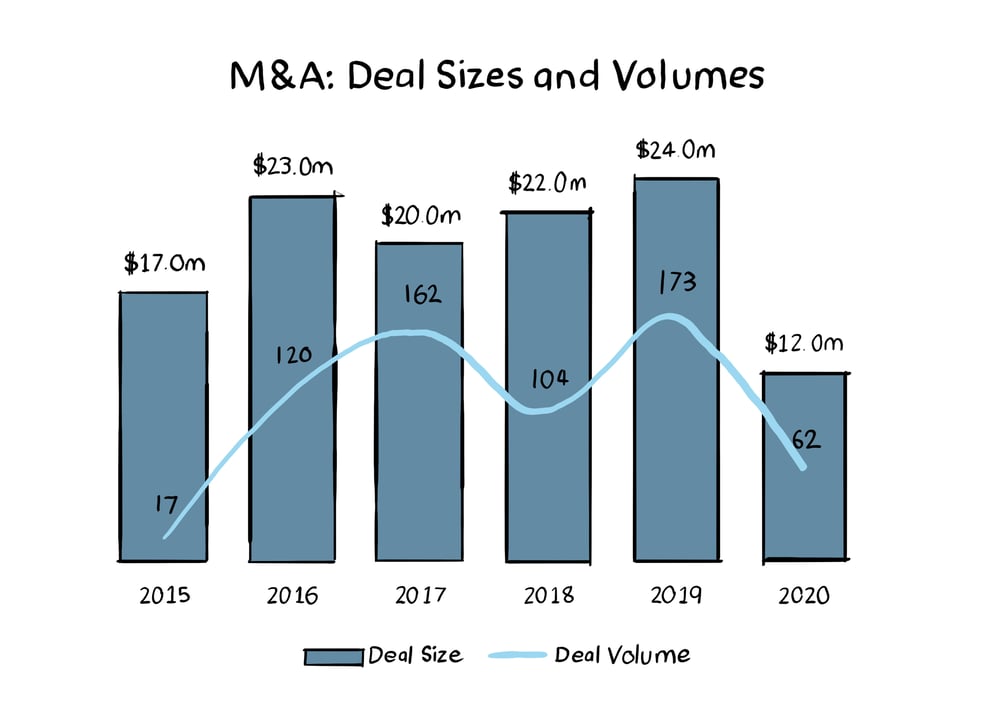

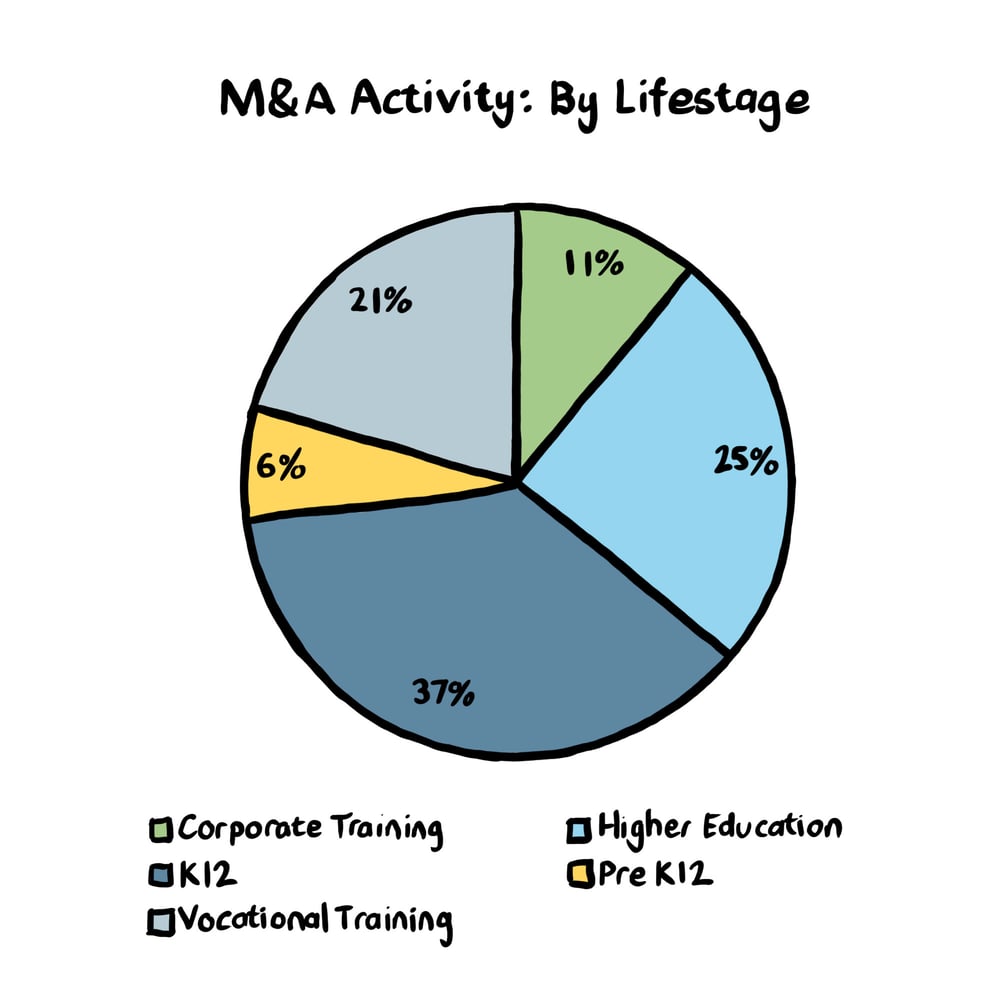

| M&A Activity > |

|

|

|

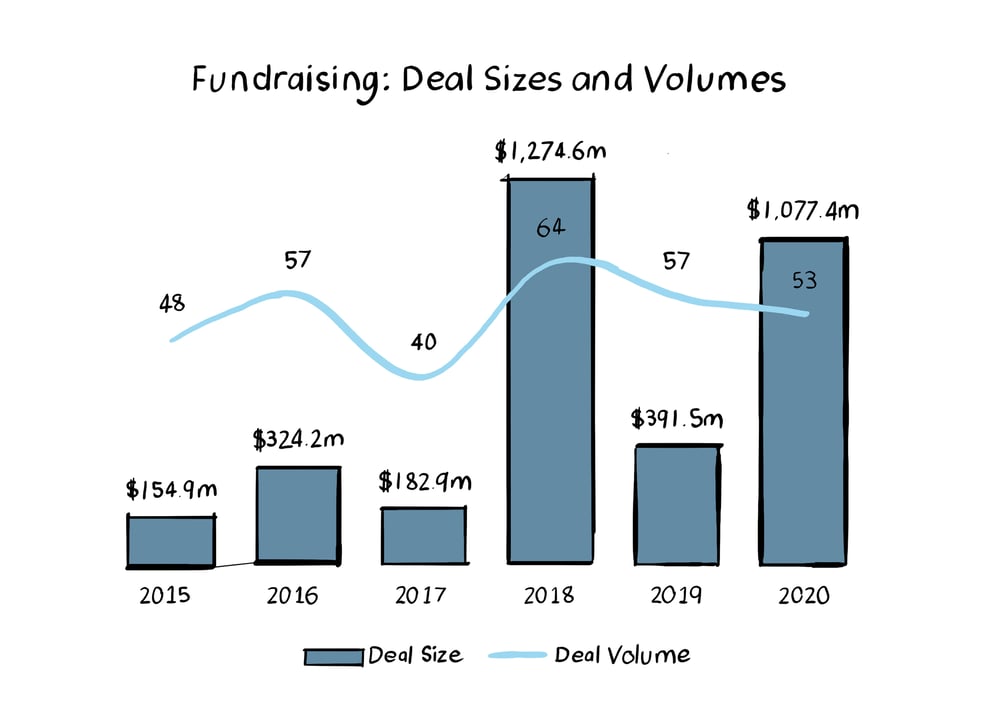

| Significant Fundraising Activity > |

|

|

|

|

|

Market Feature: India

With the largest youth population in the world, education presents both a significant challenge and a huge opportunity for India. Like many developing countries, public education suffers from poor administration and limited facilities, resulting in high drop-out rates and low quality education. This has prompted parents to look for supplementary sources of education and has driven tremendous growth in adoption of online education and other EdTech tools by Indian consumers. Given the strong demand, the market is expected to be worth a staggering $3.2 billion by 2022.

The potential of this market has attracted investors from all over the globe who have invested millions into India-focused online education providers. 2018 was a particularly strong year for fundraising, with BYJU’s scooping almost $1 billion. Despite the COVID-19 pandemic, 2020 is not far behind, again driven by BYJU’s raising $700m in the year to date. M&A deal sizes are still comparatively small, and a number of local players are using this opportunity to scale. Unacademy has been particularly active this year and has acquired 4 online education brands - Kreatryx, Prepladder, Ono Labs and Coursavy.

Successful business models seem to focus on after-school study, targeted tuition or test-prep products. Interestingly, none of the large EdTech companies are targeting the in-classroom market as yet. According to Sequoia Capital, low tech use in the classroom may be down to current products not meeting the demands of an Indian school environment, rather than due to lack of demand. 94% of Indian teachers believe the use of technology can deliver better learning outcomes, but they cited lack of time, training, or infrastructure as a barrier to adoption¹. A clear opportunity exists for EdTech providers that can customise their tools to meet the in-classroom needs of both teachers and students.

India is currently a hub of IT and business outsourcing services due to its large, skilled workforce. It could soon be an educational hub too and is positioned to be the biggest online education consumer market in a few years time. With COVID-19 further accelerating EdTech adoption, we expect to see deal activity picking up as companies compete for market share in this attractive and fast-growing sector.

¹Source: CapitalIQ; Smart Business Box; Ravishankar G V, MD Sequoia Capital

|

|

|

|

|

|

|

|

|

|