|

|

|

|

|

|

In this month's X Report, we look at finding Pedagogy Market Fit in EdTech, and explore the scale-up landscape - its activities and trends in the education market. Each month, we will share a snapshot of key trends, showcase the stars of today and tomorrow, provide some food for thought as well as mergers, acquisitions and fundraising.

|

|

|

|

|

The Need for Pedagogy Market Fit in EdTech

Mario Barosevcic - Emerge Education

Covid could not have been more kind towards EdTech. An industry that has faced slow sales cycles, hesitant consumers and investor doubts, is now the hottest industry in town.

EdTech is a very broad industry solving many different problems. In bull markets like this, it is easy to forget about one, still neglected area that more founders need to pay attention to – pedagogy and learning impact.

The first two decades of this century have been about setting up the technology foundations in the significantly underdigitised education market through software like the Learning Management System (LMS). We have digitised and improved access to content and education through apps, Massive Open Online Courses (MOOCs) and Online Programme Managers (OPMs).

With the foundations slowly developing, the last few years have seen innovations around building bridges and connectivity in education and careers through companies like Guild Education (employees < > degrees) and Handshake (students < > jobs).

However, contrary to what most people think, most EdTech to date has had very little to do with advancing and improving learning itself. Convenience and flexibility aside, online education is still worse than face to face. Most people dislike the LMS, while MOOCs and educational apps are plagued with poor engagement and completions. Pedagogy in EdTech often comes as an afterthought or when it is too late. We are still in the stone age of learning and technology.

The same way it is hard to build rockets without space engineers, it is hard to improve how the brain consumes and retains information without pedagogues and a strong understanding of the science of learning. It is great that education is becoming mobile friendly, bite-sized and more fun but we need to remember that real learning will always need to have elements of struggle that force us to actively use our brains.

Luckily, we already know a lot about pedagogy and how to create strong and lasting educational impact. All the research boils down to the need for making learning active, collaborative and applied.

When we speak with founders looking to specifically move the needle on learning impact, we like to think about the steps they are making towards achieving what we call 'Pedagogy Market Fit'. The concept is very similar to Product Market Fit with a key distinction being the emphasis on active versus passive product interaction.

Companies that achieve passive Product Market Fit in education can achieve great business successes and impact especially when acting as bridges between education and careers and supporting career progression. Frequent transactional activities or one-off milestones and events, however, are unlikely to foster strong and lasting learning impact.

Pedagogy Market Fit can be achieved when the product creates an active, meaningful learning user experience. With products that have Pedagogy Market Fit, end users are marking up materials and content, extracting insights, generating ideas, asking and answering questions, debating conclusions, repeating concepts, understanding their strengths and weaknesses, making and learning from mistakes.

Big startups that we consider as pioneers of Pedagogy Market Fit include Minerva Project (online learning platform), Lambda (project-based career learning) and Busuu (language learning).

The time is now for the next generation of founders to take EdTech to the next level by focusing on improving learning impact. Those that relentlessly pursue Pedagogy Market Fit will build strong foundations to reach global scale.

Interested in more insights about EdTech startups and scaleups? Sign up to the Emerge Education EdTech founder focused newsletter here.

|

|

|

|

|

|

The Challenge of Scaling Up

The term ‘startup’ is known the world over, however the term ‘scaleup’ is still a relatively new one. With many startups failing for one reason or another, the term serves to differentiate businesses who are still in their experimentation phase from those that have achieved proof of concept, enjoyed a degree of success and are ready to move on to the next phase of growth.

While there are a variety of definitions available that can be used to determine whether a business is regarded as having moved onto the next phase of its lifecycle – mainly referring to growth rates, employee count and revenue – scaleups can essentially be seen as successful startups.

They have a roadmap to profitability, experiment less and are better able to manage risk. They also tend to have a more defined organisational structure, as generalist founders begin handing over select responsibilities to more experienced specialists who have been brought in to help the company fulfil its potential.

Regardless of industry, it is often challenging for startups to graduate from their nascent life phase and become scaleups. This is particularly true in EdTech, which has seen a proliferation of startups entering the market in recent years. In EdTech, the product is arguably the most important determinant of whether a company can scale. While this may sound obvious, creating a product that is the right mix of intuitive, engaging and problem-solving is a tall order and one that many startups do not get quite right.

An example of a company that has successfully navigated the transition from startup to scaleup is the 2020 EdTechXGlobal Awards winner OpenClassrooms. Founded in 2007, OpenClassrooms is a French online programme manager that offers diploma training programmes and free-access courses in various fields including web development, project management, human resources and user experience. Since 2012, the company has raised $150m over five funding rounds, including an $80m Series C round in April of this year. Over this time, the company has grown their team to over 2,000 people, moved offices numerous times to accommodate this growth and added services offerings to cater to corporate clients.

Turning an idea into a profitable, scalable business is a challenge. Thousands of startups have set their sights on EdTech in recent times. For these companies, the coming years and their ability to create a product that excites consumers and can adapt to meet changing market needs will be decisive in determining whether they will be successful in mirroring the likes of OpenClassrooms in graduating and making the jump from startup to scaleup.

To find out more and apply for the 2021 EdTechX Scale-Up Awards, visit the EdTechX Awards page.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| M&A Activity > |

|

|

|

(1) Source: S&P Capital IQ

|

|

|

| Significant Fundraising Activity > |

|

|

|

|

|

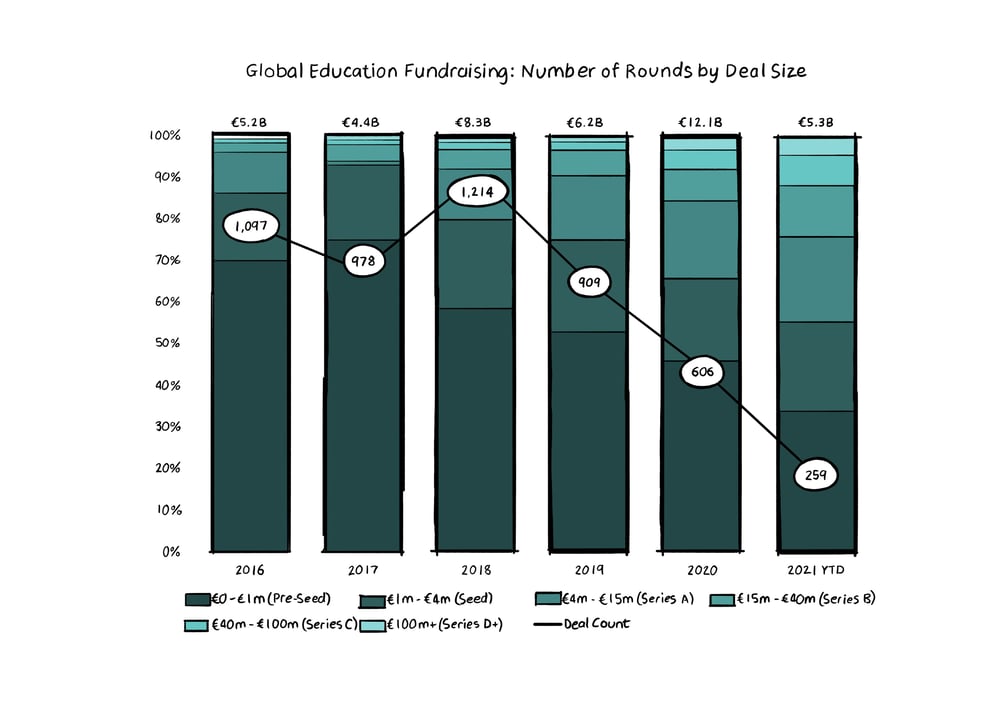

Global Education Fundraising: Number of Rounds by Deal Size 1

A key characteristic that distinguishes a scaleup from a startup is their funding. A key characteristic that distinguishes a scaleup from a startup is their funding.

Startups, while still finding their feet, will typically raise pre-seed or seed funding. This funding will typically cover the costs associated with developing their business idea, market research and product development. There are many parties keen to invest in this stage of funding, including founders, friends, family, incubators, and venture capitalists. After having developed a track record (for example, an established customer base, consistent revenue and other positive KPIs), a company may opt to raise Series A, B and C rounds in order to help them continue on their growth trajectory.

In this funding stage, companies will use the proceeds to develop their business model and product, formalise internal processes and hire more experienced executives – activities characteristic of scaleups. In fact, receiving Series A funding is a significant milestone for any startup as history suggests that fewer than 10% of companies that raise a seed round are successful in subsequently raising a Series A round.

Looking at trends in fundraising in the Education market, the above graph indicates that both deal count and the share of rounds that are pre-seed/seed have decreased over time. This suggests that EdTech companies are steadily graduating from the startup phase of their lifecycle and are becoming scaleups as the industry matures. From its peak of 93% in 2017, pre-seed/seed rounds now only account for 56% of Education fundraising rounds, with Series A now accounting for approximately 20% of rounds, up from only 1% in 2017.

An example of a company that has quickly made the step up from seed to Series A is Engageli. Founded in 2020 and headquartered in San Mateo, California, Engageli provides an engaging digital learning platform to higher education institutions. In October of last year, Engageli closed a seed round of $14.5m which included participation from several individual investors as well as Emerge Education and BRM Capital. Quickly following on from that round, the company closed their Series A fundraising round of $33m last month, taking its total capital raised to $47.5m. Their Series A round included participation from Maveron, Educapital and Corner Ventures. The capital raised in the most recent round will be used to further scale product development and fuel continued growth.

As more scaleups have emerged and progressed onto Series C rounds, we have also seen a degree of consolidation taking place – with scaleups acting as either the target for larger, more established EdTech companies, or as an acquirer of smaller startups. Kahoot! is one established EdTech firm that has been particularly active in the M&A space this year. Most recently and significantly, in May this year the company announced they had agreed a deal in principal to acquire Clever Inc. for approximately $500m. Clever provides a digital platform used by students, schools, teachers and school districts and had raised over $50m in capital from outside investors prior to the Kahoot! acquisition. The Clever deal followed Kahoot!’s $27m acquisition of employee engagement and learning platform Motimate in April this year.

The slowdown in fundraising rounds, increasing size of those rounds and consolidation point towards an industry that is slowly maturing. While the signs of a maturing industry were there even before the onset of COVID-19, the pandemic could very well act as a catalyst for the acceleration of companies making the jump from startup to scaleup. As EdTech uptake increases, investments in the sector will be more focused on those products that make a real impact on their users’ lives and we will slowly see the next generation of scaleups and unicorns emerge.

1 Source: dealroom.co

|

|

|

|

|

|

|

|

|

|