|

|

|

|

|

|

This month's X Report looks at the EdTech Unicorn landscape amid the rapid growth of the industry, and we share insights on the Brazilian EdTech market. Each month, we will share a snapshot of key trends, showcase the stars of today and tomorrow, provide some food for thought as well as mergers, acquisitions and fundraising.

|

|

|

|

|

The Rise of EdTech Unicorns

EdTech is a diverse industry that has progressed at great speed since computer assisted instruction was first used in the classroom half a century ago. Today, from teachers and pupils to government bodies and parents to employers and employees, we all use an array of digital tools to improve and facilitate teaching and learning. EdTech’s potential to effect measurable and positive social change on a wide scale has resulted in rapid growth of the industry and consequently, the birth of multiple EdTech unicorns.

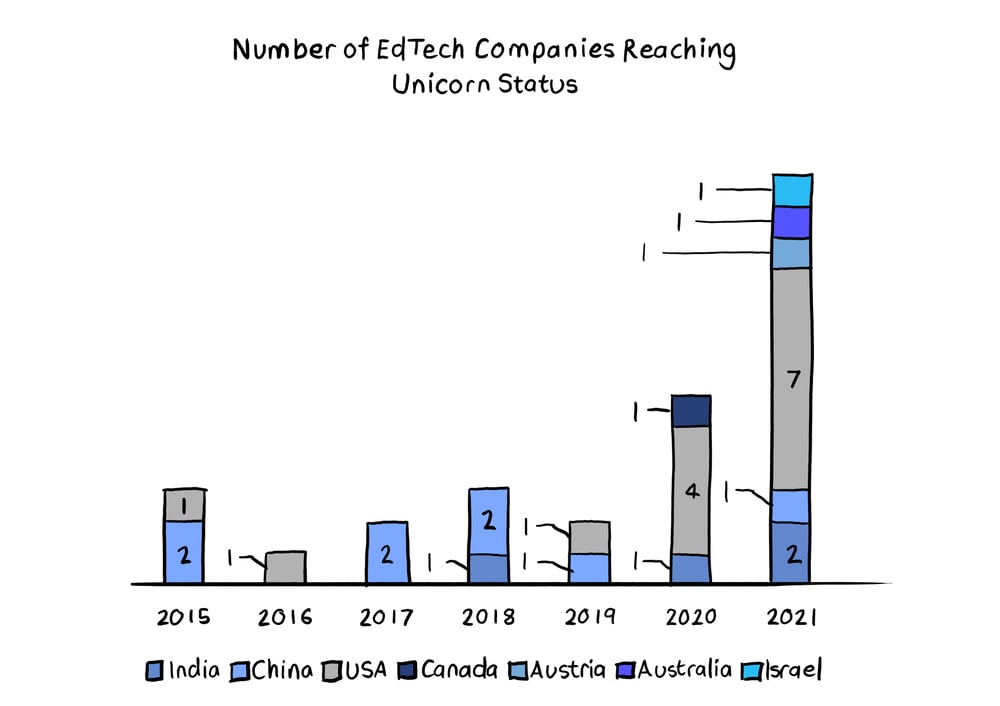

Originally coined in 2013 by venture capitalist Aileen Lee, the term “unicorn” is used to describe a privately held startup company with a billion-dollar valuation, a status so rare at the time that she chose the analogy with the mythical creature. Fast forward to 2021, which now counts more than 800 unicorns around the world, 32 of which are EdTech companies collectively valued at $92 billion having raised over $20 billion of total funding in the last decade1.

In the last 18 months, all countries have experienced significant challenges to their education systems as Covid-19 exposed shortfalls in digital infrastructure. This triggered a more pressing demand for online learning and B2C EdTech solutions, with schools, governments and parents investing in EdTech to minimise disruption to education during the pandemic. EdTech companies needed to grow quickly to meet the rising demand, and we saw twelve EdTech providers reaching unicorn status in 2021 alone. This year also saw three companies leaving the unicorn status behind following successful IPOs.

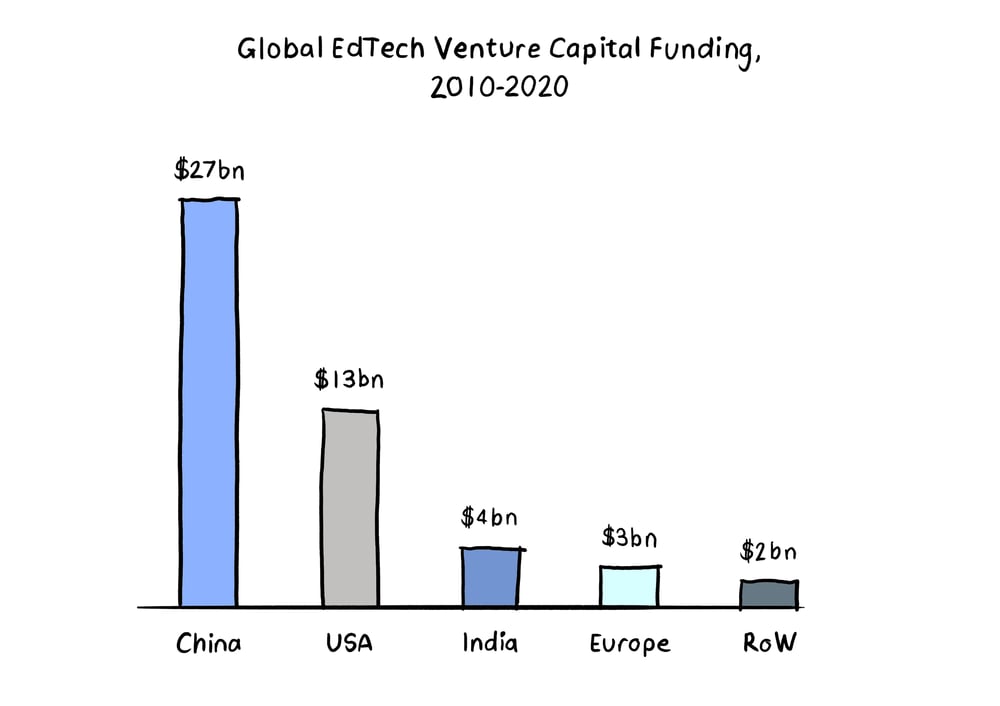

Almost all EdTech unicorns are based in North America and China, with other notable unicorns being based in India, Taiwan, Canada, Austria, Australia and Israel. The US has pioneered developments in the EdTech sphere, largely supported by the power of Silicon Valley. Similarly, China has shown much enthusiasm towards innovating and investing in EdTech. However, the Chinese Government has recently cracked down on EdTech and tutoring by way of introducing draconian rules, including forcing tutoring companies to become non-profit and halting foreign investments and IPOs.

These actions wiped out billions of dollars that domestic and foreign investors have poured into China’s innovative EdTech companies over the last few years, causing the valuations of many EdTech giants to plummet. An example is TAL Group which saw over 93% of its value wiped out, as 50 to 80% of its revenue came from tutoring (currently banned). These recent developments cast doubt over the predicted expansion of EdTech companies within China.

On the flip side, this uncertainty has created opportunities in the European EdTech scene, with European EdTech venture capital investment on course to more than double in 2021 from $711 million in 2020. In June 2021, Europe gained its first EdTech unicorn, Austrian-based GoStudent, which offers an online service that connects students with private tutors. The Company has a €1.4 billion valuation and is paving the way for others within the space.

It is evident that the hype surrounding EdTech has generated investor interest and activity, and ultimately soaring valuations. The way we live, learn and work has seen fundamental changes, laying the foundations for sustained growth in the education technology sector and fuelling the rise of EdTech unicorns.

1 Source: Holon IQ

|

|

|

|

|

EdTechs in Brazil: A promising moment

Lucia Dellagnelo - Center of Innovation for Brazilian Education (CIEB)

School closures due to the Covid-19 pandemic aggravated existing problems in the Brazilian educational system, such as learning gaps and student drop outs. On the other hand, the need to teach and learn remotely opened up for the 2.2 million Brazilian teachers and 48 million students the opportunity to use digital technologies and experiment with new ways of learning and interaction.

Under these unprecedented circumstances, companies that develop educational technologies (EdTechs) had, for the first time, the opportunity to have their digital resources massively used by students and teachers. This explains why 2020 was a positive year for the Brazilian EdTech market, despite the economic crisis caused by the pandemic.

The 2020 EdTechs Mapping Report, carried out by the Center of Innovation for Brazilian Education-CIEB in partnership with the Brazilian Startups Association, revealed a 26% increase in the number of companies in the sector compared to 2019. The survey mapped 566 active EdTech companies in Brazil, most of them located in the Southeast region and focused on basic education. In addition to the creation of new EdTechs, 63% of existing EdTech companies reported a growth in revenue in 2020.

Although the scenario looks promising, there is a list of challenges to be overcome for the full incorporation of digital technologies in Brazilian public schools. Data from Guia Edutec, a tool that maps the level of adoption of technology, shows that there is a huge variation in vision, competencies, use of digital educational resources, and infrastructure (both connectivity and devices) among Brazilian public schools.

For EdTechs, it means that comprehensive investments in digital competencies and infrastructure are urgent to consolidate the market of digital technologies in education. The main gatekeeper has been the complex and time-consuming process of public procurement which still poses difficulties for the selection and acquisition of digital educational resources with public funding.

That does not seem to prevent big players to target the Brazilian EdTech market. Recently Byju’s, the Indian EdTech unicorn, announced the start of its operation in the country, attracted by Brazil’s huge education market.

Challenges for EdTech companies to thrive in Brazil are not trivial, but the good news is that they have already been mapped out. And improving educational quality and equity is imperative for the country. EdTechs, together with the public sector, can work together to overcome obstacles and gradually transform Brazilian public education through the use of digital technology

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| M&A Activity > |

|

|

|

(1) Source: S&P Capital IQ

|

|

|

| Significant Fundraising Activity > |

|

|

|

|

|

Industry Analysis -Venture capital investment in EdTech

Key Points

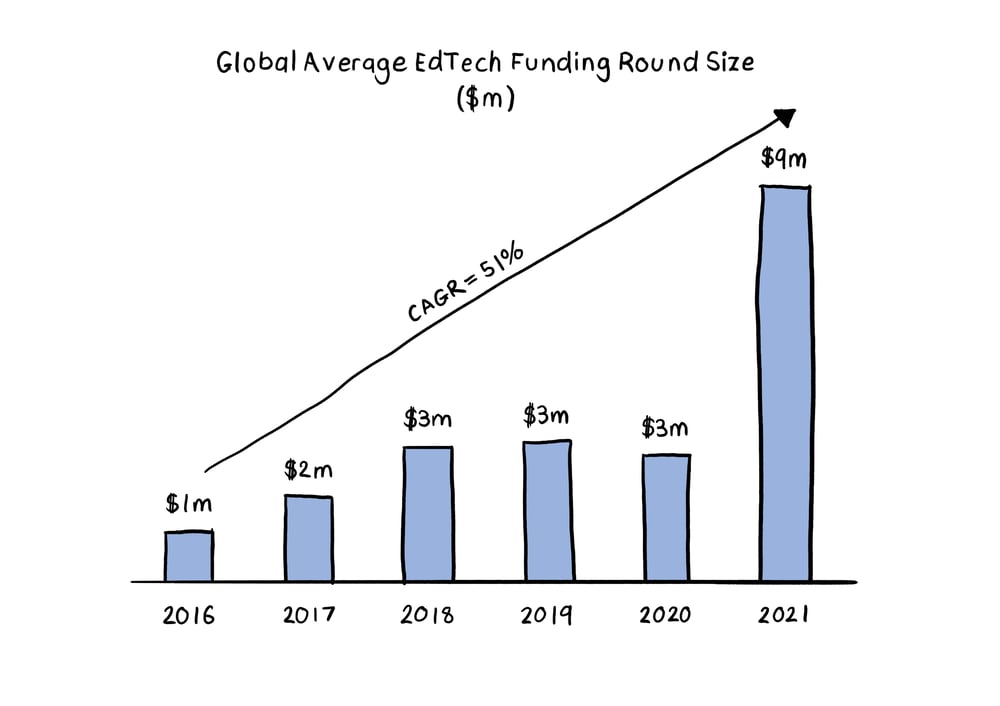

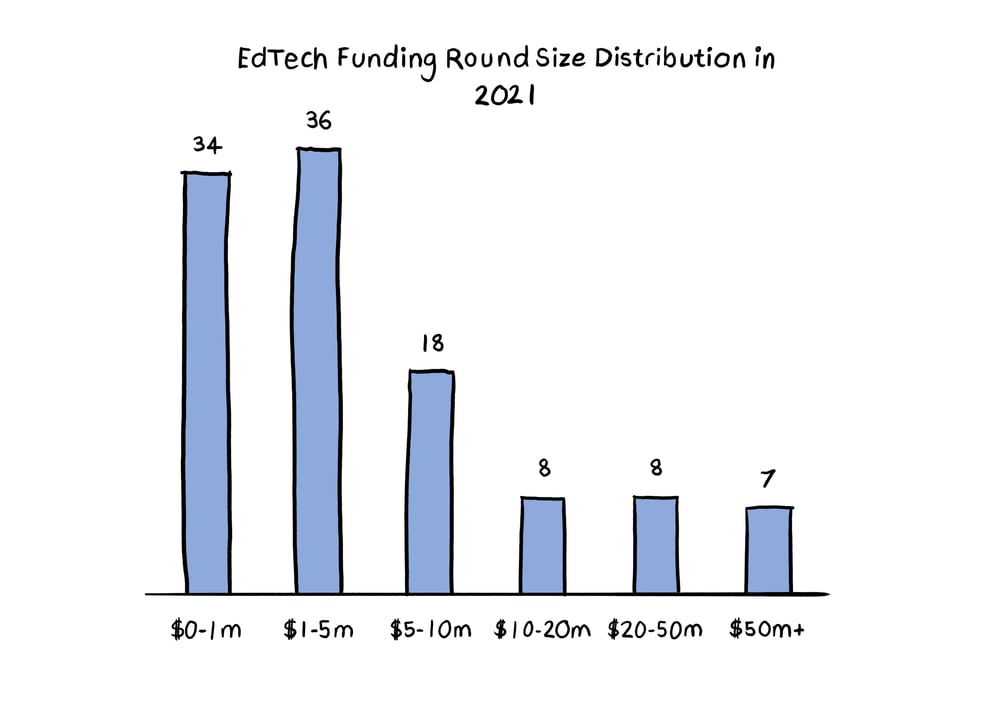

The average EdTech funding round size has grown significantly since 2016 and is expected to continue increasing as more investors show an interest in the sector. The average deal size in 2021YTD is greater than 3x the 2020 level (including rounds of all sizes). Deals in the $1-10 million range have received 49% of EdTech funding in 2021 and there is relative consistency in deal count across ranges greater than $10 million, which shows positive signs of maturity in the market. This also suggests a promising pipeline of large funding rounds in 2022. The verticals attracting the most venture capital funding are consumer EdTech (with emerging themes including digital skills and skills bootcamps) and corporate EdTech (including cybersecurity, employment support and productivity tools).

Venture capital investment in EdTech has witnessed a surge in the last 18 months, partly driven by the Covid-19 pandemic and its positive effect on the demand for alternative online learning solutions. This increase in funding has brought about a new generation of EdTech unicorns. There are currently 32 EdTech unicorns around the world, with 47% of the group having reached unicorn status in 2021. An example of a recent unicorn is Masterclass, which raised $225 million in May 2021, resulting in a valuation of $2.75 billion. The Company offers courses taught by celebrities, athletes and business leaders.

Over the past few years, Asia’s share of EdTech venture capital investment has been steadily increasing. Asian nations place a very high value on education, with a willingness and increasing ability to contribute a large proportion of household income to educating their children. China has traditionally been the largest market for EdTech funding, followed closely by the United States, who initially led the pack in terms of its collection of EdTech unicorns. United States unicorns are predominantly post-secondary focused, whilst Asian unicorns mainly operate within the K12 vertical. One notable EdTech unicorn is the Chinese live tutoring app Yuanfudao, which recently raised $2.2 billion from major Chinese and international investors, including Tencent, Hillhouse Capital and IDG Capital. The Company has successfully completed over 11 funding rounds. More recently, the world has seen the spectacular rise of India as an EdTech powerhouse. An example of arguably one of the most successful EdTech unicorns is India-based BYJU’s, which offers educational games, interactive videos and quizzes and has a valuation of $16.7 billion. The Company joined the list of EdTech unicorns in 2018 after a $100 million raise. BYJU’s has received funding from multiple investors including Blackstone Group, UBS and Eric Yuan (the founder of Zoom).

The growth profile of the EdTech industry will continue to draw venture capital investment, driving up valuations and allowing for the creation of new EdTech unicorns in the medium to long term. EdTech is an exciting space to watch, as its solutions continue to transform the way we learn while also providing an opportunity for substantial returns for investors.

|

|

|

|

|

|

|

|

|

|