|

|

|

|

|

|

In this month's X Report, we evaluate the EdTech power shift from China to India, share news on London EdTech Week and explore the upskilling & reskilling landscape in EdTech. Each month we share a snapshot of key trends, showcase the stars of today and tomorrow, offer our insight on mergers, acquisitions and fundraising, as well as providing some further food for thought.

|

|

|

|

|

Why India is the New China

Hilary Foord, Investment Banking Analyst at IBIS Capital

For the most part of the last decade, China has been the hottest EdTech market leading the industry’s technological advancements and innovation. Chinese tutoring firms alone attracted $6.5bn of funding in 2020 across 32 deals, at the time cementing its status as EdTech’s leading geographical market. However, regulation introduced by the Chinese government in 2021 changed this. A law was introduced banning EdTech companies that teach school curriculum from making profits, raising capital, or going public. These measures not only crippled China’s tutoring market but also removed investor confidence (both public and private) from China’s EdTech scene. Larry Chen, the founder of GSX Techedu, personally lost over $14bn of his own fortune.

However, India is perfectly placed to take advantage of this situation. Investors will look to re-deploy their capital into another market. Since the Chinese regulation came into place, 4 Indian EdTech firms have achieved Unicorn status in the form of UpGrad (the online pathway programme provider), Eruditus (executive level course platform), Vedantu (online tutoring firm), and just recently in May 2022 PhysicsWallah (online tutoring platform). These 4 firms join Byju’s (now a decacorn) and Unacademy in becoming Indian unicorns. The sudden glut of Indian unicorns emerging, whilst slightly coincidental, highlighted the EdTech power shift that had occurred. In fact, 2021 was the first year that India attracted more EdTech investment than China. $3.8bn was invested into India up from $2.3bn in 2020 compared to $2.7bn into China down from $10.2bn in 2020.

There are a number of macro-economic trends that favour continued growth within India which will help it to maintain its status as Asia’s brightest EdTech market. India’s youthful population is an attractive option for education companies to benefit from. 26% of its population are younger than 15 and the country’s median age is 28. The adoption of the internet is also growing rapidly in India. According to the IAMAI-Kantar ICUBE 2020 report, India had 622 million active internet users in 2020. This number is expected to increase by 45% to reach 900 million by 2025, with rural India particularly driving this growth. Coupled with this, smartphone ownership is accelerating as ownership among government school student families increased from 30% in 2018 to 56% in 2020 and from 50% to 74% among private school student families. Rising affluence in India is helping to underpin these trends - forecast real GDP per capita growth is expected to be 9% per annum through 2022. These macro-economic trends have seen bullish predictions for the industry in India. The Indian EdTech sector is projected to be a $10.4bn industry by 2025 and to reach $30bn by 2030 growing at a CAGR of 15% over this period.

According to analytics company Tracxn, there are several other Indian EdTech companies rising the ranks. Tracxn has predicted that India has 15 active ‘soonicorns’, including student financing firm Leap Finance, online coding school BrightChamps, and Teachmint, the teaching and classroom management platform, highlighting that the future is bright for India. It seems that India will not be giving up its mantle of Asia’s leading EdTech market anytime soon!

|

|

|

|

|

London EdTech Week | 20 to 26 June 2022

Celebrate the Now and Next of learning and work

London EdTech Week 2022 will be the 4th edition of our connected, collaborative week-long celebration of learning innovation and the future of work across London. Welcoming over 5,000 global attendees, London EdTech Week is the UK’s flagship 7-day EdTech celebration featuring diverse events powered by EdTechX’s co-chairs, partners and other leaders in the EdTech community. It is a unique and open platform that welcomes any member of the global learning ecosystem to create collaborative, connected events across London, celebrating the Now and Next of learning and work.

2022 will see a fantastic, varied schedule with 30+ community-led workshops, networking events, product launches, cocktails, field trips and more, kicking off with the official opening reception on Monday 20th June hosted by AWS, Brighteye Ventures and MindCET- EdTech Innovation Center for an evening of catching up with the community and getting ready for a week packed with edtech action.

London EdTech Week is all about networking with likeminded stakeholders, meeting the founders, academics, investors and policy makers of the education industry, learning from EdTech experts, and even showcasing your skills. With guest speakers and thought-provoking panels, you’ll hear from key figures in the education sector, explore the challenges facing the industry and learn about the opportunities to better serve our global education systems.

From a hands-on introduction to UX design and coding, to exploring the current edtech fundraising landscape, from ideation and product launch to maximising your company’s educational impact goals, and from workforce development to how to build your career in tech, there will be events for everybody. At the heart of the week is our flagship Summit, EdTechX - bringing together 700+ decision-makers for a day of networking and thought-leadership on 23 June.

LETW Co-Chairs: AND Digital, BESA, Brighteye Ventures, Cooley, EdTechX Holdings, Google Cloud, IBIS Capital, UCL EdTech Labs

LETW Hosts: AWS, BrainStation, EdTech Garage, GoldStarEd, Igloo Vision, MIndCET, National Taiwan Normal University, UCL IOE Faculty of Education and Society, Ufi Ventures & Tyton Partners, Virtual Internships, WISE, Fox Williams

You can explore the full list of confirmed events and register your interest in these on the London EdTech Week website.

Tickets to the EdTechX Summit include access to all open London EdTech Week events, so book your All Access ticket now to celebrate London EdTech Week and EdTechX!

EdtechX Holdings pioneers investment in the “eduverse” with zSpace Inc.

EdTech & Future of Work SPAC, EdtechX Holdings Acquisition Corp II (NASDAQ:EDTX) is pleased to announce its Business Combination with zSpace Inc., a US leader of augmented and experiential content (AR/VR) technology solutions for education (K12) and workforce development, with the support of a $25M anchor investment from GII and Kuwait Investment Authority.

EdTechX Holdings is a proud pioneer of the #SPACsForGood pledge, which is an invitation to other SPAC teams to pledge a percentage of their founder shares to support endowments and non-profit initiatives around education, health, the environment, diversity and tech inclusion.

Watch this video to find out more about zSpace's leading technology. See the full press release HERE.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| M&A Activity > |

|

|

|

| Significant Fundraising Activity > |

|

|

|

|

|

The Upskilling & Reskilling Landscape in EdTech

Key Points

According to Monster's Future of Work report for 2022, 91% of employers are struggling to fill positions because of a skills gap. The digital shift brought about by the pandemic has shown that the IT and technical skills gap is now wider than ever, and filling this gap has become a priority for employers and job-seekers alike. The race to fill the skills gap has not gone unnoticed by the investment world and since last year, investors have poured more than $2.1bn into an assortment of EdTech startups offering solutions to this growing problem. Primarily, they are focused on two areas: upskilling, which provides skills to grow in one’s current career, and reskilling, which involves training for an entirely new job. The World Economic Forum estimates that 50% of employees will need to be reskilled by 2025.

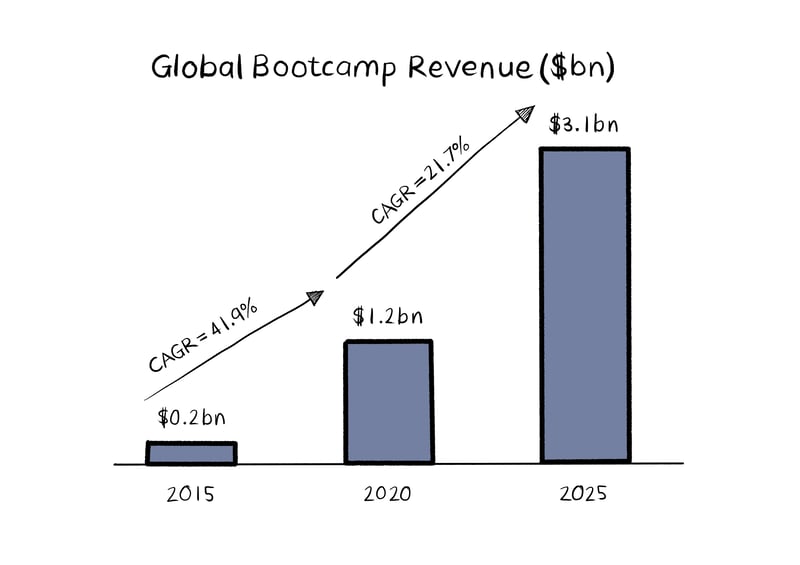

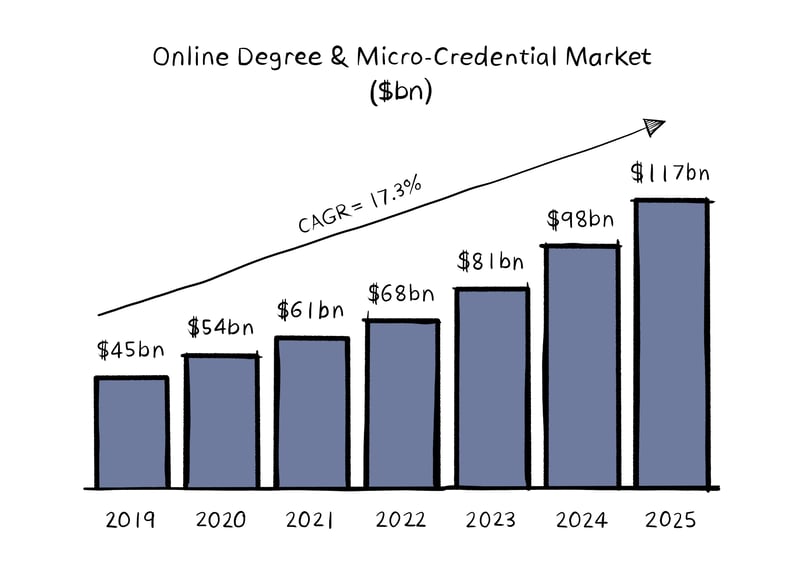

A popular model within the skilling1 vertical is tech bootcamps. These digital or technical programs are full-time, intensive skills training sessions that typically last 9 to 12 weeks. In 2021, over 100,000 professionals were reskilled and upskilled through tech bootcamps globally. This figure is expected to reach over 380,000 by 2025, and represents over $3 billion of expenditure. This next generation bootcamp market will cater to B2C,B2B and university and government partnerships. Going forward, the bootcamp landscape will consist of increasingly global and more diverse cohorts. Further to this, OPM platforms and apprenticeship players will also be considered part of the future bootcamp ecosystem. With the significance of college degrees continuing to decrease in the hiring process, the prevalence of bootcamps and digital credentials is gaining momentum and therefore growing the demand for degree alternatives. Consequently, alternative and micro-credentials are making up an important part of the upskilling landscape. With the online degree and micro-credential market expected to reach $117 billion by 2025, we can expect to see further embedding of alternative credentials within existing qualification frameworks.

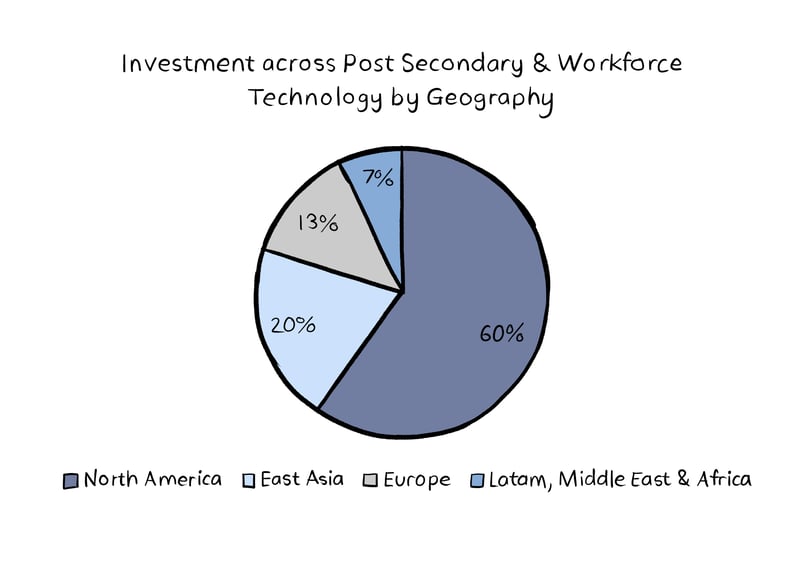

Due to this consistent funding flow, startups offering individuals the opportunity to build their skillsets have seen robust growth. One such startup, is California-based upskilling platform Degreed. The Company offers a learning platform that allows individuals and organisations to build skills and certify their expertise. Degreed has raised a total of $411.8 million, and investors include Owl Ventures, GSV Ventures and AllianceBernstein. From a geographic perspective, North America dominates the post-secondary and workforce technology2 space, accounting for 60% of investment. East Asia accounts for 20% of the investment across post- secondary and workforce technology. This regions share of investment is likely to increase rapidly, as the World Economic Forum has identified India to have the second-highest additional employment potential through upskilling. Due to this consistent funding flow, startups offering individuals the opportunity to build their skillsets have seen robust growth. One such startup, is California-based upskilling platform Degreed. The Company offers a learning platform that allows individuals and organisations to build skills and certify their expertise. Degreed has raised a total of $411.8 million, and investors include Owl Ventures, GSV Ventures and AllianceBernstein. From a geographic perspective, North America dominates the post-secondary and workforce technology2 space, accounting for 60% of investment. East Asia accounts for 20% of the investment across post- secondary and workforce technology. This regions share of investment is likely to increase rapidly, as the World Economic Forum has identified India to have the second-highest additional employment potential through upskilling.

It is evident that there is a growing need for upskilling and reskilling within the workplace. We can expect to see increased investor interest within the space, as more and more organisations invest in the upskilling of their employees, in order to better meet their company’s needs. Alternative credentials, such as bootcamps and online degrees, offer individuals the chance to acquire in-demand skills in a shorter time frame than the traditional university route, and at a fraction of the cost. As a result, exponential growth is predicted within this vertical, as upskilling and reskilling cement their place within EdTech.

1 Includes upskilling and reskilling

2 Includes TalentTech, HR Tech & JobTech

|

|

|

|

|

|

|

|

|

|