|

|

|

|

|

|

|

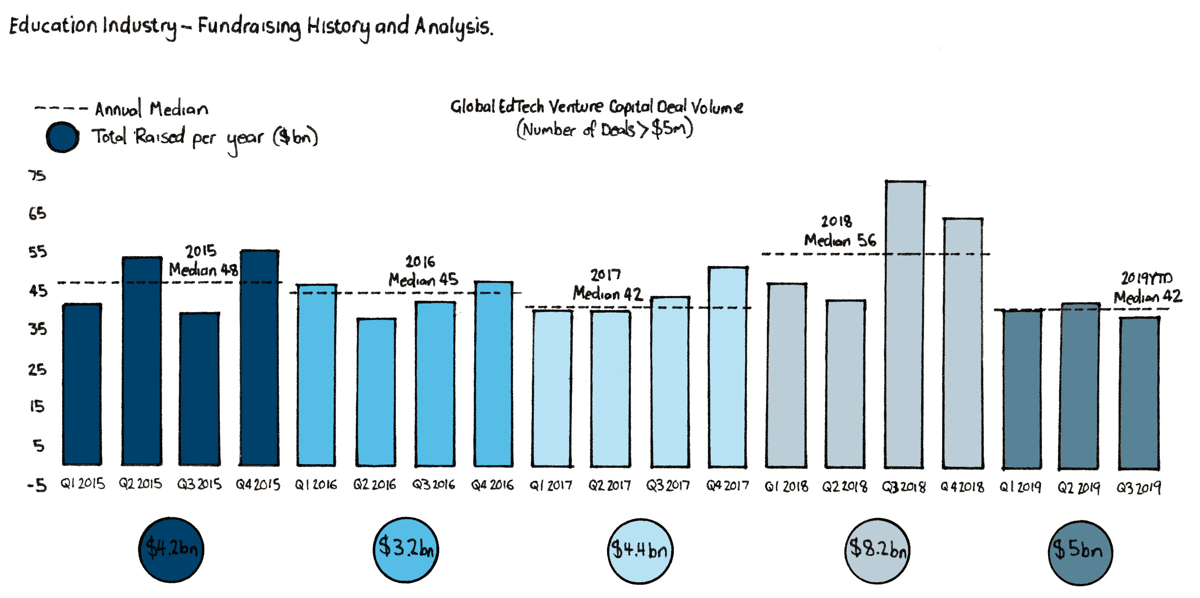

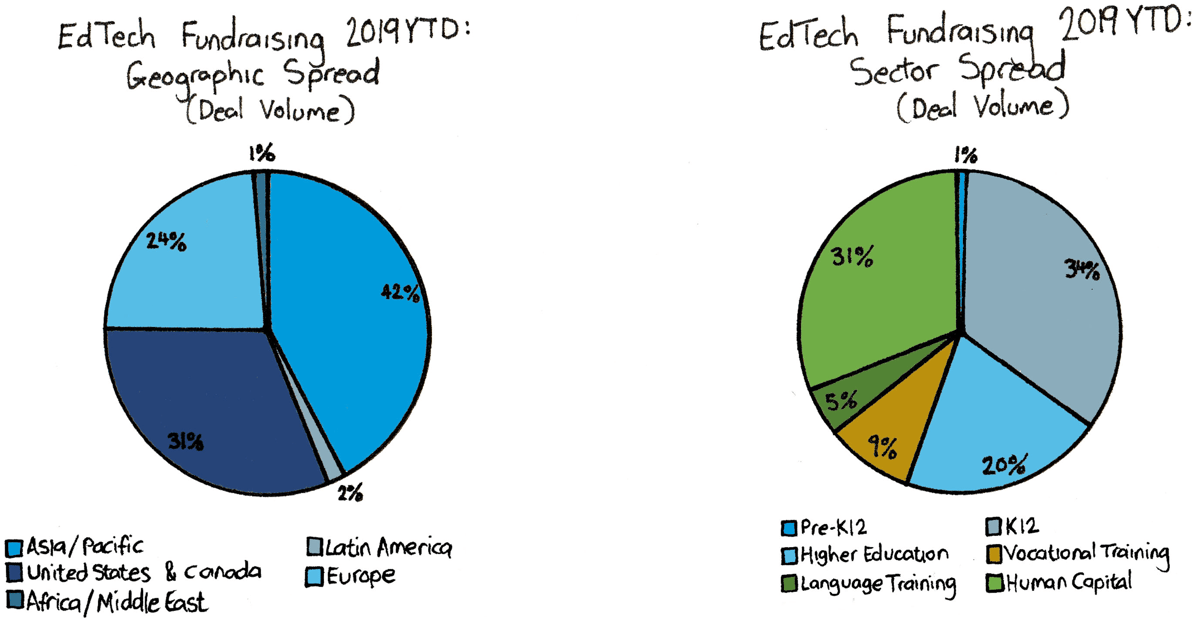

For the final instalment of 2019, we discuss the four day working week, emerging markets in Asia as well as comparing Q3 performance in the sector. The report aims to provide you with a bite-sized summary of what is happening in the world of learning and training.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|